Understanding Your Motorcycle Loan

Buying a motorcycle is an exciting milestone, whether it's your first cruiser, a nimble sportbike, or a long-haul tourer. However, the financing process can often be as complex as the machine itself. Our Motorcycle Payment Calculator is designed to cut through the confusion, giving you a clear picture of your monthly obligations before you even step foot in a dealership.

Unlike car loans, motorcycle loans often come with different terms, higher interest rates, and unique insurance requirements. This tool helps you factor in all the variables—including trade-ins, sales tax, and dealer fees—so you can budget with confidence.

How to Use This Calculator

Getting an accurate estimate takes just a few seconds. Here's a breakdown of the inputs:

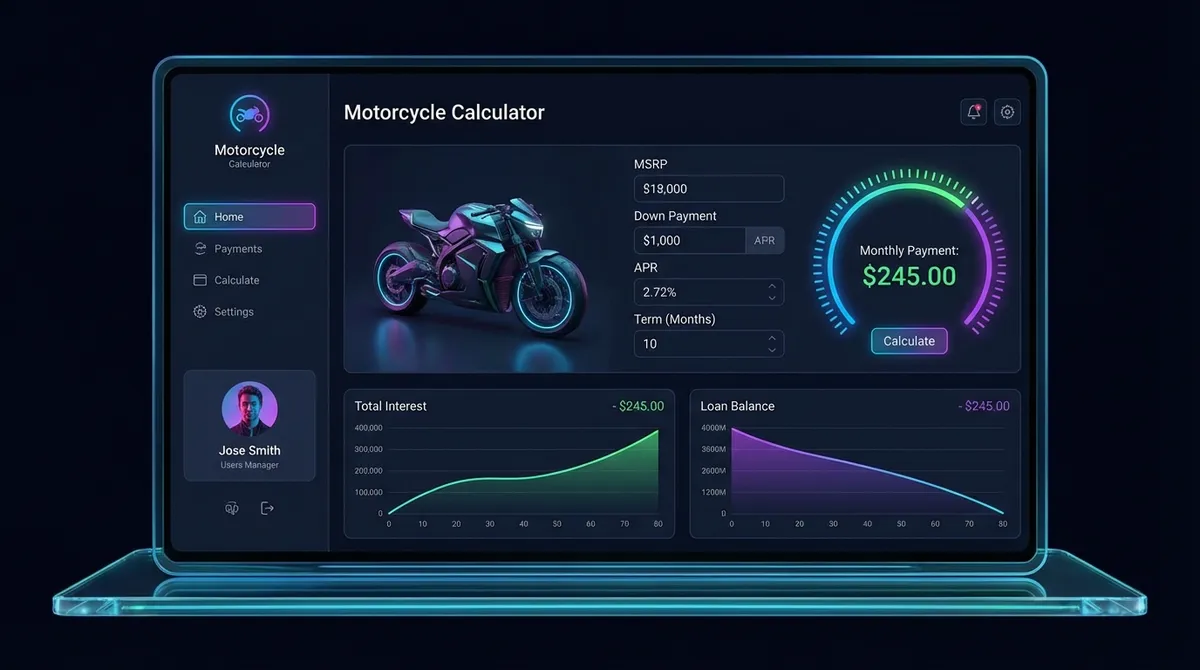

- Vehicle Price: The negotiated price of the motorcycle. Don't forget to negotiate!

- Trade-in Value: The amount the dealer is offering for your old bike. This acts as a down payment and often reduces the sales tax you pay.

- Down Payment: Cash you are putting upfront. A higher down payment reduces your loan amount and monthly payment.

- Interest Rate (APR): The annual percentage rate of your loan. This depends on your credit score and the bike's age.

- Loan Term: How long you have to pay off the loan. Common terms are 36, 48, or 60 months.

- Sales Tax: Your state's sales tax rate. This is a significant cost often overlooked.

- Fees: Title, registration, and dealer documentation fees. These can add $300-$800 to your total cost.

Motorcycle Financing vs. Auto Loans

It's important to understand that financing a motorcycle is different from financing a car. Lenders often view motorcycles as "luxury items" or "recreational vehicles," which can lead to:

- Higher Interest Rates: Rates for bikes are typically 1-3% higher than auto loans for the same credit tier.

- Shorter Terms: While 72 or 84-month loans are common for cars, motorcycle loans are usually capped at 60 months to prevent you from being "upside-down" (owing more than the bike is worth) due to depreciation.

- Higher Insurance Costs: Full coverage insurance is required for financed bikes and can be expensive, especially for sportbikes.

Hidden Costs of Ownership

Your monthly loan payment is just one part of the equation. When budgeting for a bike, you must also consider the "hidden" costs that don't appear on the loan agreement:

- Gear: A good helmet, jacket, gloves, and boots can easily cost $500-$1,000+.

- Maintenance: Motorcycle tires wear out much faster than car tires (often every 3,000-10,000 miles) and valve adjustments can be pricey.

- Insurance: As mentioned, premiums vary wildly. Always get an insurance quote before you buy the bike.

- Storage: If you don't have a garage, you might need to pay for winter storage or a secure parking spot.

Tips for Getting the Best Rate

To keep your monthly payment low, follow these tips before applying for a loan:

- Check Your Credit: Know your score. A score above 700 will qualify you for significantly better rates.

- Shop Around: Don't just take the dealer's financing. Check with local credit unions, which often have the best rates for motorcycles.

- Put Money Down: Aim for at least 10-20% down. This lowers your risk to the lender and can qualify you for a lower tier of interest rates.

- Consider a Personal Loan: For cheaper used bikes (under $5,000), a personal loan might be easier to get, though the rate might be slightly higher.

- Compare APR, Not Just Monthly Payment: A longer loan term lowers the monthly number but inflates total interest. Use our APR Calculator to see the true cost of different rate and term combinations before signing anything.

Frequently Asked Questions

For more information on motorcycle values and pricing, visit J.D. Power (NADA Guides) or check safety ratings at the NHTSA Motorcycle Safety page.