Understanding Boat Loans: A Complete Guide

Buying a boat is a dream for many, offering the freedom to explore open waters and create lasting memories. However, unless you're paying cash, navigating the waters of marine financing can be as complex as navigating a busy harbor. Our Boat Loan Calculator is designed to help you estimate your monthly payments and understand the total cost of ownership before you commit.

Unlike auto loans, boat loans often have longer terms, different down payment requirements, and unique tax implications. This guide will walk you through everything you need to know about financing a boat, from interest rates to hidden costs.

How to Use This Calculator

To get the most accurate estimate, you'll need to gather a few key figures. Here's how to use each field:

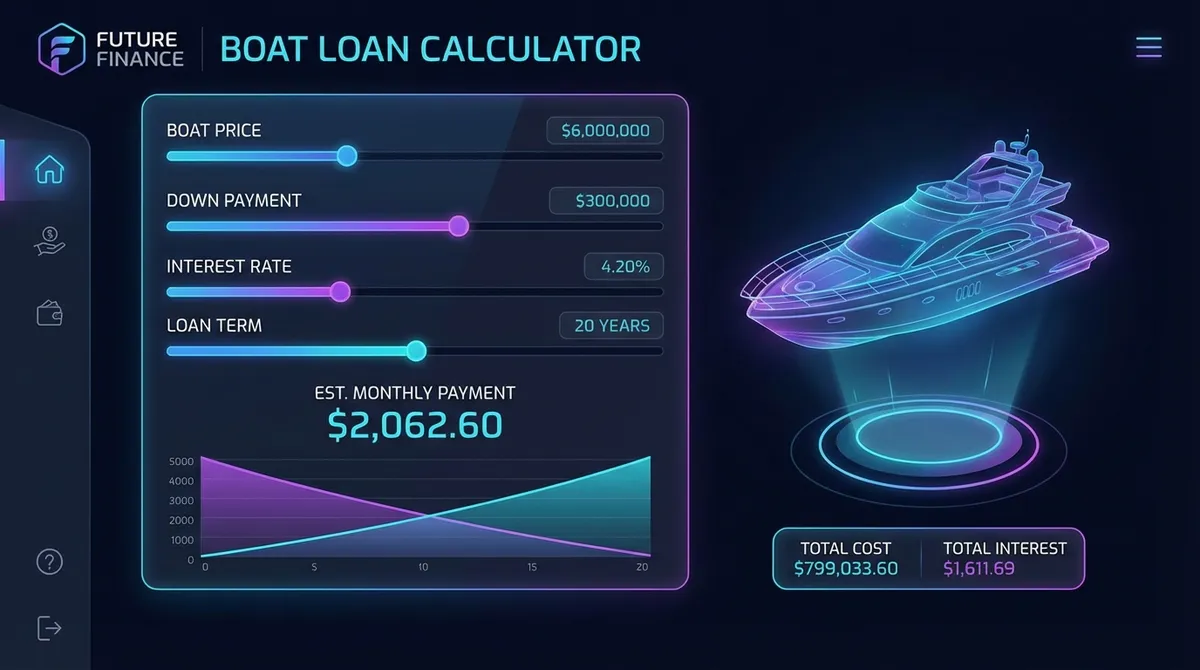

- Boat Price: The total negotiated price of the vessel, including the engine and trailer if applicable.

- Down Payment: The amount of cash you're putting upfront. Lenders typically require 10-20% down for boat loans.

- Trade-In Value: If you're trading in an older boat, enter its value here. This reduces your taxable amount in many states.

- Sales Tax: Your local sales tax rate. Don't forget this, as it can add thousands to your loan.

- Interest Rate (APR): The annual percentage rate for your loan. Boat loan rates are generally higher than auto loans but lower than personal loans.

- Loan Term: The length of the loan in months. Boat loans can range from 60 months (5 years) to 240 months (20 years) for larger vessels.

Boat Loans vs. Auto Loans: Key Differences

While the math is similar, the terms of marine financing differ significantly from car buying:

- Longer Terms: Because boats depreciate slower than cars, lenders offer longer terms—often up to 15 or 20 years for loans over $100,000. This keeps monthly payments lower but increases total interest paid.

- Larger Down Payments: Expect to put down at least 10-20%. Zero-down boat loans are rare and usually come with much higher interest rates.

- Strict Underwriting: Lenders view boats as luxury items (the first thing people stop paying in a recession), so credit score requirements are often stricter (typically 700+ for the best rates).

These same recreational-lending rules apply across powersports. If you're also weighing an off-road purchase, our ATV loan calculator shows how four-wheelers and side-by-sides carry an even steeper rate premium than boats over comparable auto loans, and our jet ski loan calculator breaks down what a personal watercraft costs once you fold in the trailer and a short riding season.

Hidden Costs of Boat Ownership

Your monthly loan payment is just the beginning. When budgeting for a boat, you must account for the "hidden" costs that can easily equal or exceed your loan payment:

- Storage & Docking: Marina slips can cost $10-$30 per foot per month. Dry storage or trailer storage is cheaper but still adds up.

- Fuel: Boats are thirsty. A day on the water can easily burn $100-$500 in fuel depending on the vessel size and usage.

- Maintenance: The rule of thumb is to budget 10% of the boat's value annually for maintenance (cleaning, winterizing, engine service).

- Insurance: Marine insurance varies widely based on cruising area and boat type.

The largest hidden cost isn't on that list at all — it's depreciation. A new fiberglass powerboat sheds around 20% of its value in year one and 6-9% annually after that, which on a $45,000 purchase quietly costs more per month than fuel and insurance combined. Our boat depreciation calculator projects your resale value year by year so you can compare it against your projected loan balance before you pick a term.

Tax Benefits: The Second Home Deduction

Here's some good news: If your boat has a sleeping berth, a galley (kitchen), and a toilet, it may qualify as a second home for tax purposes. This means you could potentially deduct the interest paid on your boat loan, similar to a mortgage interest deduction.

Consult with a tax professional to see if you qualify, as this can significantly offset the cost of ownership. For more details, check the IRS Publication 936 regarding home mortgage interest.

Tips for Getting the Best Boat Loan Rate

- Check Your Credit: Ensure your credit score is in top shape before applying. A score above 740 usually unlocks the "prime" rates.

- Shop Around: Don't just take the dealer's financing. Check with credit unions, banks, and specialized marine lenders.

- Consider the Age: Financing for older boats (20+ years) can be difficult or require a marine survey.

- Marine Survey: For used boats, always get a marine survey. It's like a home inspection for a boat and can save you from buying a lemon.

Frequently Asked Questions

For more information on safe boating and regulations, visit the U.S. Coast Guard Boating Safety website.