Understanding Boat Loans: A Deep Dive

The allure of the open water is undeniable. Whether it's a sleek speedboat for weekend thrills, a pontoon for family gatherings, or a sailboat for quiet escapes, buying a boat is a significant lifestyle investment. However, unlike buying a car, navigating the waters of marine financing can be a bit more complex. Our Boat Payment Calculator is designed to cut through the confusion, giving you a clear picture of your potential monthly costs so you can focus on the horizon, not the bottom line.

Financing a boat is often compared to a hybrid between a car loan and a mortgage. While the application process feels like buying a car, the terms, down payments, and tax implications can resemble buying a second home. This guide will walk you through everything you need to know to use our calculator effectively and secure the best financing for your vessel.

How to Use This Calculator

We've built this tool to be as intuitive as possible, but understanding each input will ensure the most accurate estimate:

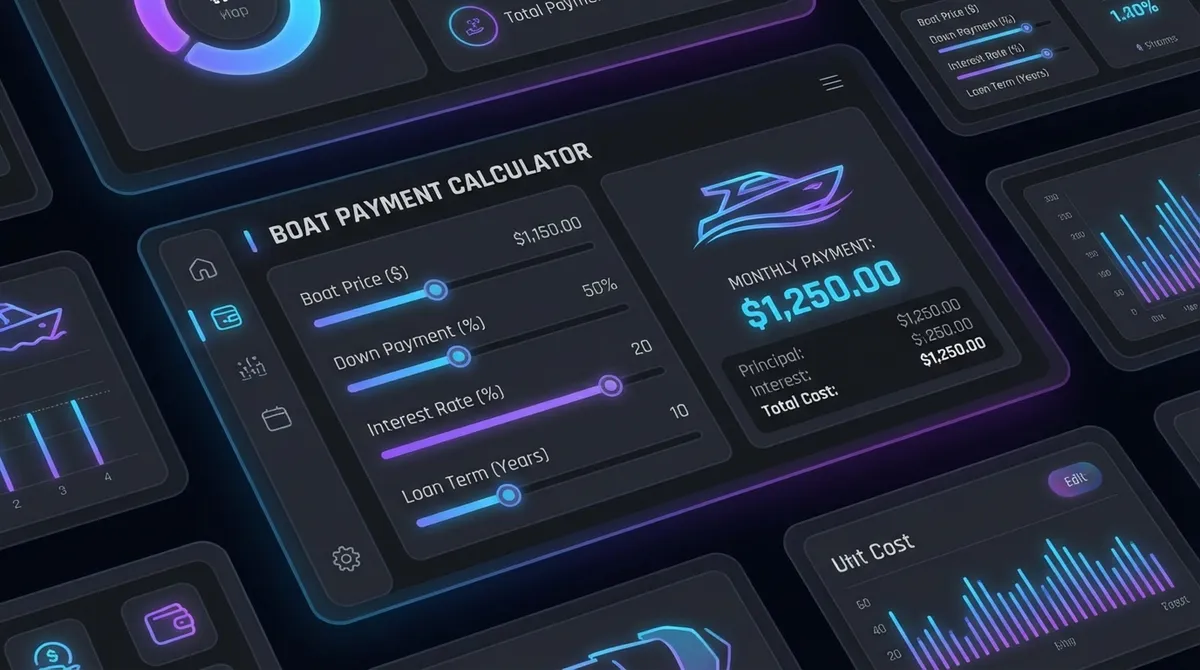

- Boat Price: The negotiated purchase price of the vessel. Don't forget to include the cost of the trailer and engine if they are priced separately, as is common with some new boats.

- Down Payment: Marine lenders typically require a larger down payment than auto lenders. Expect to put down 10% to 20%. A larger down payment not only lowers your monthly bill but also improves your chances of approval.

- Trade-In Value: If you're upgrading, enter the value of your current boat here. This reduces the taxable amount in many states, saving you money upfront.

- Sales Tax: Boat sales tax varies significantly by state and sometimes even by county. Some states have a cap on boat tax (e.g., Florida has a cap on discretionary sales surtax, but not the state 6%). Be sure to look up your local marine tax laws.

- Interest Rate (APR): Rates for boat loans are generally higher than auto loans but lower than personal loans. They depend heavily on your credit score, the loan term, and the age of the boat.

- Loan Term: This is where boats differ from cars. Terms can range from 5 to 20 years (60 to 240 months). Longer terms mean lower monthly payments but significantly more interest paid over the life of the loan.

Boat Financing 101: What You Need to Know

Before you sign on the dotted line, it's crucial to understand the landscape of marine lending. Unlike auto loans, which are relatively standardized, boat loans can vary significantly depending on the age of the vessel, the loan amount, and the lender's specific requirements. Knowing the nuances of secured loans, tax implications, and marine surveys can save you thousands of dollars and help you avoid common pitfalls during the buying process.

1. Secured vs. Unsecured Loans

Most boat loans are secured, meaning the boat itself is collateral. This allows lenders to offer lower interest rates and longer terms (up to 20 years for expensive vessels). Unsecured personal loans are an option for smaller, older, or less expensive boats, but they come with higher rates and shorter terms (usually maxing out at 5-7 years).

2. The "Second Home" Tax Deduction

Here is a financial perk unique to boats: If your vessel has a sleeping berth, a galley (kitchen), and a toilet (head), the IRS may consider it a "second home." This means you might be able to deduct the interest on your boat loan, just like a mortgage. This can result in significant savings at tax time, effectively lowering the "real" cost of your loan. Always consult a tax professional to confirm your eligibility.

3. Marine Surveys

For used boats, especially larger ones, lenders will almost always require a marine survey. Think of this as a home inspection for a boat. A certified surveyor checks the hull, engine, and systems for issues. If the survey reveals problems, the lender may refuse to finance the boat until they are fixed, or they may lower the loan amount.

The Hidden Costs of Boat Ownership

The monthly loan payment is just the tip of the iceberg. Experienced boaters often cite the "10% Rule": expect to spend 10% of the boat's value annually on operating costs. When budgeting, you must account for:

- Storage/Docking: Marina slips can cost hundreds or thousands of dollars a month depending on location and boat size. Dry stack storage or a trailer in your driveway are cheaper alternatives.

- Fuel: Boats are thirsty. A day on the water can easily burn $100-$300 in fuel for a powerboat.

- Insurance: Marine insurance varies by cruising area (e.g., hurricane zones cost more) and boat type.

- Maintenance: "Boat" stands for "Break Out Another Thousand" for a reason. Saltwater environments are harsh, and regular maintenance is non-negotiable to preserve value and safety.

- Winterization: If you live in a cold climate, you'll need to pay for hauling, shrink-wrapping, and engine winterization every year.

And then there's the cost nobody invoices you for: lost resale value. A typical powerboat gives up 40% or more of its purchase price over the first five years, which works out to roughly $300 a month on a $45,000 boat. Run your specific hull type through our boat depreciation calculator to see the year-by-year curve before you commit to a payment.

Pro Tips for Getting the Best Rate

Want to lower that monthly payment? Follow these tips before applying:

- Check Your Credit: Marine lenders are strict. A score above 700 is often required for the best rates.

- Buy Newer: Lenders offer better rates and longer terms for new or late-model boats. Financing a 20-year-old boat often requires a higher rate and a shorter term.

- Shop Specialized Lenders: Don't just ask your local bank. Marine lenders understand boats better and often offer more competitive terms than general banks.