The Ultimate Guide to Leasing vs. Buying a Car

One of the most common and perplexing questions in the automotive world is: "Should I lease or buy my next car?" It’s a debate that has raged for decades, with passionate advocates on both sides. The truth is, there is no single "right" answer. The best choice depends entirely on your financial situation, driving habits, and personal preferences. (For a deep dive, read our guide on Leasing vs. Buying Strategies for 2025).

Our Lease vs. Buy Calculator is designed to cut through the noise and provide you with a clear, mathematical comparison of the two options. By analyzing the total net cost of ownership over a specific period, you can see exactly which path makes the most financial sense for you. But beyond the numbers, it's crucial to understand the fundamental differences between leasing and buying.

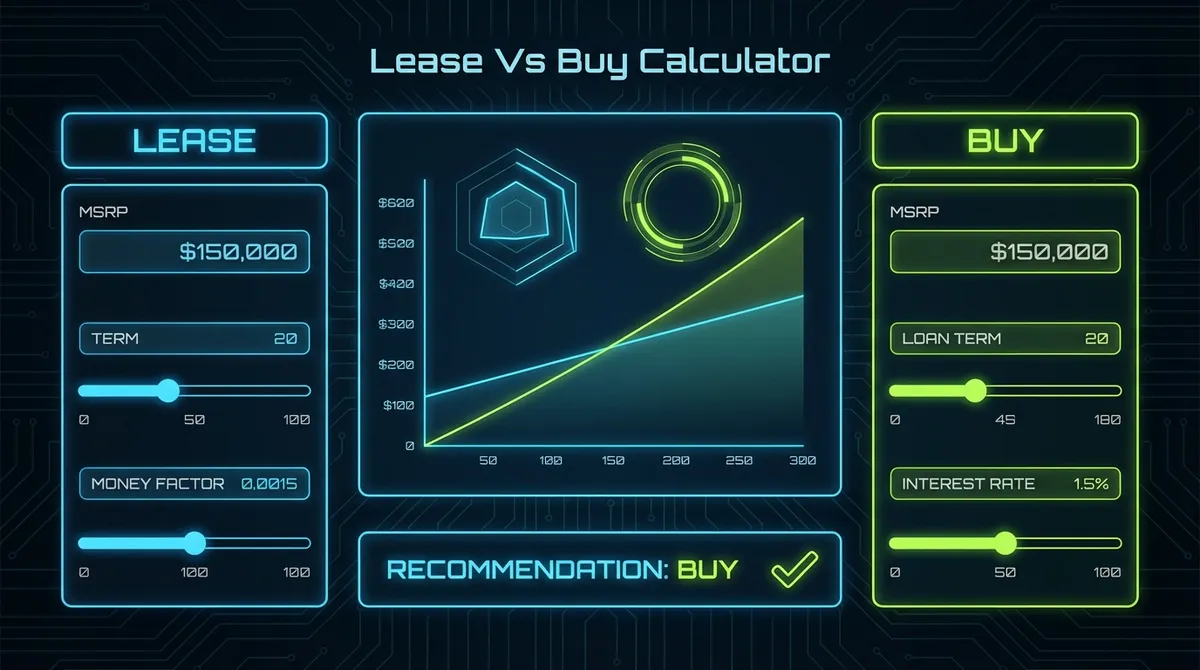

How to Use This Calculator

To get the most accurate comparison, you'll need to gather some specific numbers. Here's a step-by-step guide to using our tool:

- Vehicle Price & Tax: Enter the negotiated price of the car (not just the MSRP) and your local sales tax rate. This forms the baseline for both calculations.

- Buying Details: Input your planned down payment, the loan term (e.g., 60 months), the interest rate (APR), and the estimated resale value of the car at the end of the comparison period.

- Leasing Details: Enter the lease specific inputs: your down payment (capitalized cost reduction), the lease term (e.g., 36 months), the money factor (or equivalent APR), the residual value (usually a percentage of MSRP), and any acquisition or disposition fees.

- Compare: Hit the "Compare Options" button. The calculator will project the costs for both scenarios over the lease term (since that is the shorter, defining period) and show you the "Net Cost" of each.

Leasing vs. Buying: The Core Differences

At its heart, the difference between leasing and buying comes down to ownership.

- Buying means you pay for the entire cost of the vehicle, plus interest if you finance it. Once the loan is paid off, you own the car free and clear. You can keep it for ten years, sell it, or trade it in. You build equity.

- Leasing is essentially a long-term rental. You are paying for the depreciation of the car during the time you use it, plus a "rent charge" (interest). At the end of the lease, you return the car and walk away (or buy it for the residual value). You generally do not build equity.

Pros and Cons of Leasing

Pros of Leasing

- Lower Monthly Payments: Since you only pay for depreciation, payments are often 30-60% lower than buying.

- New Car Every Few Years: You always drive a late-model vehicle with the latest safety and tech features.

- Warranty Coverage: The car is usually under factory warranty for the entire lease term, minimizing repair costs.

- No Resale Hassle: You don't have to worry about selling the car or trade-in values; just drop off the keys.

Cons of Leasing

- No Ownership/Equity: You make payments for years but own nothing at the end. It's a perpetual expense.

- Mileage Limits: Leases have strict mileage caps (e.g., 10k-12k miles/year). Exceeding them costs dearly (15-25 cents/mile).

- Wear & Tear Charges: You must return the car in excellent condition or pay for scratches, dings, and tire wear.

- Hard to Terminate: Breaking a lease early is extremely difficult and expensive.

Pros and Cons of Buying

Pros of Buying

- Ownership & Equity: Every payment builds equity. Once paid off, your monthly car expense drops to zero.

- Unlimited Mileage: Drive as much as you want without penalty. Great for long commutes or road trips.

- Freedom to Modify: You can customize the car, tint windows, or upgrade the sound system as you please.

- Long-Term Savings: Buying and holding a car for 7-10 years is almost always the cheapest option. Our lease vs finance calculator shows the exact break-even point where financing starts saving you money over serial leasing.

Cons of Buying

- Higher Monthly Payments: You are paying off the entire principal, so payments are significantly higher.

- Depreciation Risk: If the car's value drops faster than expected (e.g., due to an accident or market shift), you lose money.

- Repair Costs: Once the warranty expires, you are responsible for all repairs and maintenance.

- Selling Hassle: You have to deal with selling the car or negotiating a trade-in value when you want to upgrade.

The Math Behind the Comparison

To fairly compare leasing and buying, we have to look at the Net Cost over the same period. Since leases have a fixed term (e.g., 3 years), we use that as our window.

The Lease Calculation

The cost of leasing is straightforward:Net Lease Cost = (Monthly Payment × Term) + Down Payment + Fees

Since you return the car at the end, you have no asset left, so your total expense is just the sum of all cash outflows. For a detailed breakdown of how each lease payment component is calculated, try our car lease payment calculator. And if you have the cash on hand, paying all of those lease outflows as one upfront check earns a money factor discount — our one-pay lease calculator shows whether that single-pay route beats paying monthly.

The Buy Calculation

The cost of buying is more complex because you have an asset (the car) at the end:Total Cash Out = (Monthly Loan Payment × Term) + Down Payment + TaxEquity = Car Market Value - Remaining Loan BalanceNet Buy Cost = Total Cash Out - Equity

If the car is worth more than you owe, that equity reduces your "Net Cost". If you are "underwater" (owe more than it's worth), your net cost increases.

Strategic Tips for Your Decision

Here are some expert tips to help you decide and save money regardless of which path you choose:

- Negotiate the Price First: Whether leasing or buying, the "Capitalized Cost" or "Purchase Price" is negotiable. Don't let a dealer tell you "lease prices are fixed." Negotiating the price down lowers your payments in both scenarios.

- Check the Money Factor: In leasing, the interest rate is called the "Money Factor." Multiply it by 2,400 to get the approximate APR. If the dealer quotes a money factor of 0.0025, that's 6% APR. Make sure it's competitive with current auto loan rates.

- Understand Your Mileage: Be realistic. If you drive 15,000 miles a year, do not sign a 10,000-mile lease to save $20/month. The overage penalties (often $0.25/mile) will cost you $3,750 at the end! Run the numbers with our lease mileage calculator before signing.

- Gap Insurance: Essential for leasing (often included) and highly recommended for buying with a low down payment. It covers the difference if your car is totaled and you owe more than it's worth.

For more detailed information on the legal aspects of leasing, visit the Consumer Financial Protection Bureau. You can also check Consumer Reports for their latest analysis on the lease vs. buy debate.