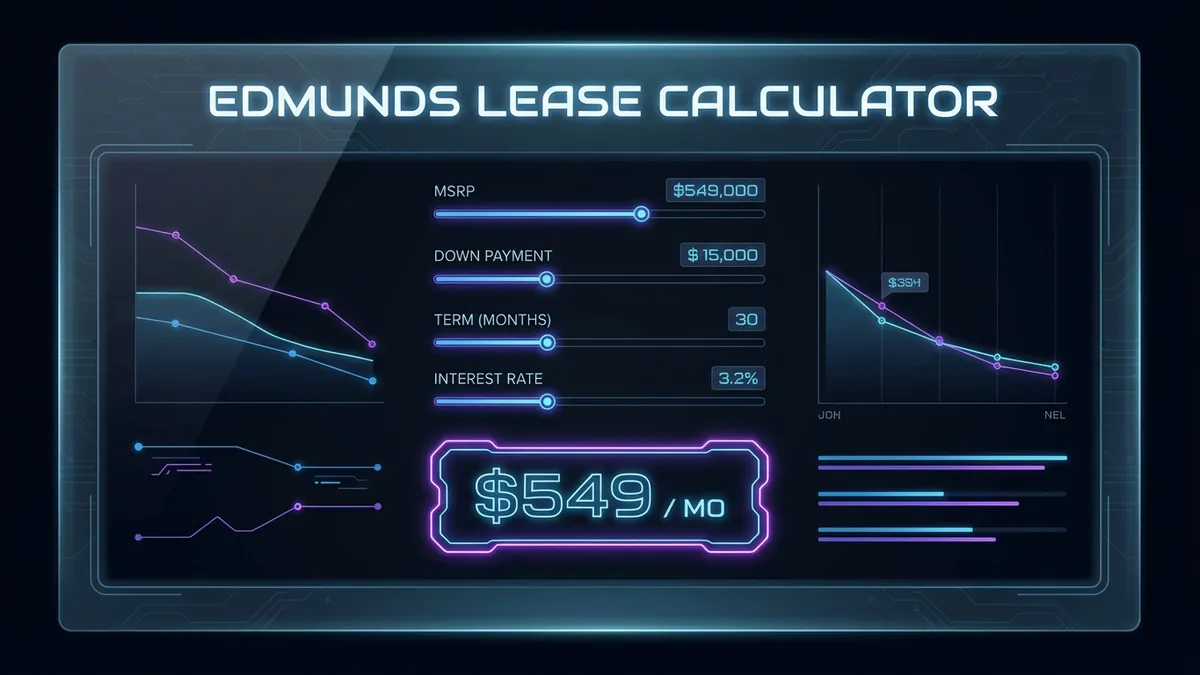

Mastering the Edmunds Lease Calculator: Your Ultimate Guide

Leasing a car can be one of the most confusing financial transactions you'll ever encounter. With terms like "money factor," "residual value," and "capitalized cost" thrown around, it's easy to feel overwhelmed. That's where the Edmunds Lease Calculator comes in. This powerful tool cuts through the jargon and provides you with a clear, accurate estimate of your monthly payments and total lease costs.

Whether you're eyeing a sleek new luxury sedan or a practical family SUV, understanding how your lease payment is calculated is the key to negotiating a better deal. In this comprehensive guide, we'll walk you through every aspect of the lease calculation process, explain the hidden fees dealers don't want you to know about, and show you exactly how to use our calculator to save thousands on your next vehicle. For more official information on leasing terms, you can visit the Consumer Financial Protection Bureau.

How to Use This Calculator

Our calculator is designed to be as intuitive as possible, but leasing math is inherently complex. Here is a step-by-step breakdown of each input field to ensure you get the most accurate results. You can also cross-reference terms with Investopedia's definition of Capitalized Cost.

- MSRP (Manufacturer's Suggested Retail Price): This is the "sticker price" of the car. You can find this on the window sticker or the manufacturer's website. It's the starting point for all lease calculations.

- Selling Price (Capitalized Cost): This is the price you actually negotiate with the dealer. Pro Tip: Never pay MSRP! Your goal is to negotiate this number down as much as possible before mentioning you want to lease.

- Down Payment (Cap Cost Reduction): Cash you pay upfront to reduce the amount you're financing. While it lowers your monthly payment, we generally recommend putting as little down as possible on a lease (more on that later).

- Trade-In Credit: The value of your current vehicle if you're trading it in. This acts like a down payment.

- Term (Months): The length of the lease. Standard terms are 24, 36, or 48 months. 36 months is the "sweet spot" for most warranties and residual values.

- Money Factor: This is the interest rate, but presented in a confusing decimal format (e.g., 0.0025). To convert it to an APR, multiply by 2400. For example, 0.0025 x 2400 = 6% APR.

- Residual Value (%): The percentage of the MSRP the car is expected to be worth at the end of the lease. This is set by the bank and is usually non-negotiable. Higher is better!

- Sales Tax (%): Your local sales tax rate. In most states, tax is added to the monthly payment, but some states (like Texas or Virginia) tax the full vehicle price upfront.

Deconstructing the Lease Formula

To truly master the Edmunds Lease Calculator, you need to understand the math happening behind the scenes. A lease payment is actually composed of three distinct parts:

1. Depreciation Fee

This is the largest portion of your payment. You are paying for the value the car loses during the time you drive it.Depreciation = (Net Cap Cost - Residual Value) / Term

2. Finance Fee (Rent Charge)

This is the interest you pay to the leasing company for using their money to buy the car. It's calculated on the average balance of the car over the lease term.Finance Fee = (Net Cap Cost + Residual Value) * Money Factor

3. Taxes

Taxes vary significantly by state. In most jurisdictions, you pay sales tax on the sum of the Depreciation and Finance Fee.Monthly Tax = (Depreciation + Finance Fee) * Tax Rate

Leasing vs. Buying: Which is Right for You?

The decision to lease or buy depends on your financial goals, driving habits, and lifestyle. If you're considering buying instead, check out our Auto Loan Calculator to compare monthly payments. Let's compare the two:

Pros of Leasing

- Lower Monthly Payments: Since you're only paying for the depreciation, lease payments are typically 30-40% lower than loan payments for the same car.

- New Car Every Few Years: You're always driving a late-model vehicle with the latest safety and tech features.

- Warranty Coverage: Most leases coincide with the factory warranty, meaning you rarely pay for repairs.

- No Resale Hassle: At the end of the lease, you just hand the keys back. No need to worry about selling a used car.

Cons of Leasing

- Mileage Limits: Leases come with strict mileage caps (usually 10k-15k miles/year). Exceeding them results in hefty penalties.

- No Equity: You don't own the car. At the end of the term, you have nothing to show for your payments unless you buy it out.

- Wear and Tear Fees: You must return the car in pristine condition or pay for scratches, dings, and tire wear.

- Higher Insurance: Leasing companies often require higher liability limits than state minimums.

5 Common Leasing Mistakes to Avoid

Even savvy buyers can get tripped up by the complexities of leasing. Avoid these pitfalls to ensure you get the best deal:

- Focusing Only on Monthly Payment: Dealers love to ask "What payment do you want?" This allows them to manipulate the numbers (by extending the term or asking for a larger down payment) to hit your target while hiding a bad deal. Always negotiate the Selling Price first.

- Putting Too Much Money Down: If your leased car is totaled or stolen in the first month, that down payment is gone forever. Gap insurance covers the bank, not you. Aim for $0 down if possible.

- Ignoring the Money Factor: Dealers often mark up the money factor to make extra profit. Always ask for the "Buy Rate" money factor and compare it to the manufacturer's base rate (check forums like Edmunds).

- Underestimating Mileage: It's cheaper to buy extra miles upfront (usually $0.15-$0.20/mile) than to pay the penalty at the end (often $0.25/mile). Be realistic about your driving habits.

- Not Checking for Rebates: Manufacturers often offer "Lease Cash" or incentives that are different from purchase rebates. Ensure all applicable rebates are applied to your Capitalized Cost.

Advanced Tip: The 1% Rule

A quick rule of thumb to determine if a lease deal is "good" is the 1% Rule. If the monthly payment (with $0 down) is less than 1% of the MSRP, it's a great deal.

- Great Deal: Payment is < 1.0% of MSRP

- Good Deal: Payment is 1.0% - 1.2% of MSRP

- Average Deal: Payment is 1.2% - 1.5% of MSRP

- Bad Deal: Payment is > 1.5% of MSRP

For example, on a $50,000 car, a payment under $500/month is excellent, while anything over $750 is likely poor value.