Unlock Savings with Car Loan Refinance Calculators

Managing an auto loan can be one of the most significant ongoing expenses in your monthly budget. However, many drivers are unaware that they might be overpaying for their car loan. This is where Car Loan Refinance Calculators become essential tools. By evaluating your current loan against potential new offers, you can uncover opportunities to lower your interest rate, reduce your monthly payment, or shorten your loan term.

Our comprehensive guide and premium calculator are designed to empower you with the data you need to make smart financial decisions. Whether your credit score has improved since you bought your car, or market interest rates have dropped, refinancing could save you thousands of dollars over the life of your loan. This article explores how to effectively use these calculators, the benefits of refinancing, and strategies to secure the best possible deal.

How to Use Our Car Loan Refinance Calculator

Using a refinance calculator is the first step in determining if switching lenders is the right move for you. Our tool is built to be intuitive and precise. Here is a step-by-step guide to getting the most out of it:

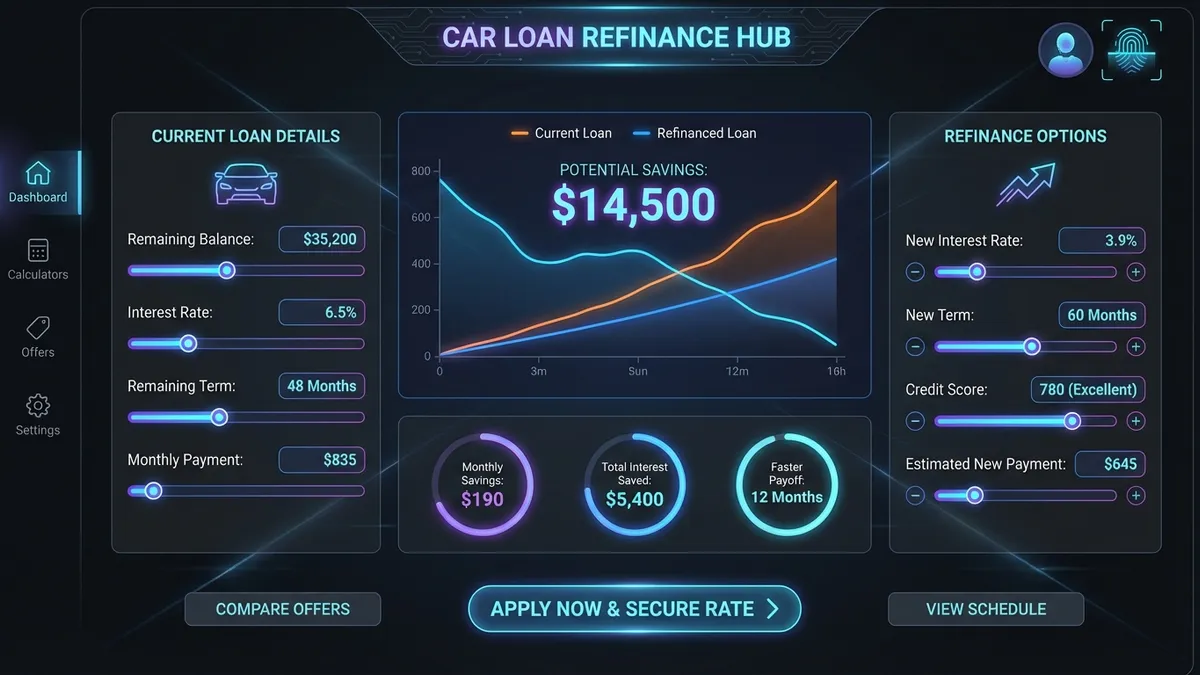

- Gather Your Current Loan Data: Before you start, find your latest loan statement. You will need your Current Loan Balance (the exact payoff amount is best, but the current balance works for estimates), your Current Interest Rate (APR), and the Remaining Months left on your term.

- Enter Current Details: Input these figures into the "Current Loan Details" section of the calculator. Accuracy here is key to getting a realistic comparison.

- Input New Loan Scenarios: In the "New Loan Offer" section, enter the New Interest Rate and New Term you are considering. You can find current average rates online or use a pre-qualified offer from a lender.

- Account for Fees: Refinancing often comes with costs, such as title transfer fees or origination fees. Use the "Refinance Fees" slider to include these costs in your calculation. This ensures you see the net savings, not just the gross interest difference.

- Review the Analysis: The calculator will instantly generate a breakdown of your Monthly Savings and Total Interest Savings. Use the interactive charts to visualize how the new loan structure compares to your current one over time.

Why You Should Consider Refinancing Your Car Loan

Refinancing is essentially replacing your existing car loan with a new one, typically from a different lender. The new loan pays off the old one, and you start making payments to the new lender. But why go through the trouble? Here are the primary motivations:

1. Lowering Your Interest Rate

The most common reason to refinance is to secure a lower Annual Percentage Rate (APR). If your credit score has improved since you first financed your vehicle, you likely qualify for better rates. Even a 1% or 2% drop in your interest rate can translate to significant savings. For example, on a $25,000 loan, reducing the rate from 8% to 5% can save you hundreds of dollars in interest per year.

2. Reducing Monthly Payments

If your budget is tight, refinancing can help free up cash flow. By extending your loan term, you can spread the remaining balance over more months, drastically lowering your monthly bill. However, be cautious: while your monthly obligation decreases, extending the term often means paying more in total interest over the life of the loan.

3. Shortening the Loan Term

Conversely, if you are in a better financial position now than when you bought the car, you might want to pay off your debt faster. Refinancing to a shorter term (e.g., going from 48 months remaining to a new 36-month loan) will increase your monthly payment but will save you a substantial amount in interest and get you title-in-hand sooner.

When is the Best Time to Refinance?

Timing is everything when it comes to refinancing. Here are the ideal scenarios to use Car Loan Refinance Calculators to check your options:

- Your Credit Score Has Improved: If you've been making on-time payments and paying down other debts, your credit score has likely risen. Lenders reserve their best rates for borrowers with excellent credit (typically 720+).

- Interest Rates Have Dropped: Economic factors influence auto loan rates. If the Federal Reserve cuts rates or the broader market trends downward, it's a prime time to check if current rates are lower than what you locked in years ago.

- You Didn't Shop Around Initially: Many buyers accept the dealership's financing offer without comparing it to other lenders. Dealer rates are often marked up. If you didn't shop around then, shopping around now could reveal much better offers from credit unions or online banks.

- Your Financial Situation Has Changed: Whether you need to lower expenses due to a job change or want to aggressively pay down debt due to a raise, refinancing allows you to restructure your debt to match your current reality.

Strategic Tips for a Successful Refinance

To maximize the benefits of refinancing, follow these expert strategies. By taking a proactive approach and understanding the nuances of the lending market, you can secure a deal that significantly improves your financial standing and helps you reach your goals faster.

Shop Around and Compare Offers

Don't settle for the first offer you receive. Use Car Loan Refinance Calculators to test offers from multiple sources. Credit unions often have lower rates than big banks, and online-only lenders can be very competitive. Most lenders offer a "pre-qualification" process that does a soft credit pull, allowing you to see potential rates without hurting your credit score.

Watch Out for Fees and Penalties

Always read the fine print. Some original loans have prepayment penalties that charge you for paying off the loan early. If this penalty exceeds your potential savings, refinancing might not make sense. Additionally, the new loan may have origination fees or title transfer fees (usually charged by your state DMV). Ensure these costs are factored into your savings calculation.

Avoid "Upside-Down" Refinancing

If you owe more on your car than it is currently worth (negative equity), refinancing can be difficult. Some lenders may still approve you but might require a cash down payment to cover the difference. Be careful not to roll negative equity into a new loan, as this perpetuates the cycle of debt.

Frequently Asked Questions (FAQ)

Here are answers to some of the most common questions drivers have about using car loan refinance calculators and the refinancing process in general. We have compiled these inquiries to help you navigate the complexities of auto financing with confidence and ensure you have all the information needed to make the best decision for your financial future.

Does refinancing hurt my credit score?

Refinancing involves applying for a new loan, which typically requires a "hard inquiry" on your credit report. This can cause a minor, temporary drop in your score (usually less than 5-10 points). However, if you shop around within a short window (typically 14-45 days), most credit scoring models treat multiple inquiries for the same type of loan as a single inquiry. Long-term, replacing a high-interest loan with a more manageable one can improve your financial health and credit score.

Can I refinance a car loan with bad credit?

Yes, but it is more challenging. Some lenders specialize in "subprime" refinancing. However, the rates offered may not be significantly lower than your current rate. It is crucial to use a calculator to verify that the new offer actually saves you money after accounting for any fees. If the savings are negligible, it might be better to focus on improving your credit score first.

Is there a limit to how many times I can refinance?

Technically, there is no legal limit to how many times you can refinance. However, each refinance resets the loan term (unless you specifically choose a shorter one) and involves fees. Constantly extending your loan term can lead to paying significantly more interest in the long run and staying in debt longer than the car's useful life.

What documents do I need to refinance?

To streamline the process, have the following ready: your driver's license, proof of insurance, proof of income (pay stubs or tax returns), vehicle registration, and details of your current loan (lender name, account number, and payoff amount).

Additional Resources

For more unbiased information on auto loans and consumer rights, we recommend consulting these government and non-profit resources: