Quick Summary

Our Used Car Calculator helps you estimate monthly payments, total interest, and the overall cost of financing a pre-owned vehicle. By adjusting the vehicle price, down payment, trade-in value, and interest rate, you can find a loan structure that fits your budget.

Introduction to Used Car Financing

Buying a used car is a smart financial move for many drivers. With new car prices reaching record highs, pre-owned vehicles offer a more affordable entry point into car ownership. However, financing a used car comes with its own set of variables that differ from new car loans. Interest rates are typically higher, loan terms may be shorter, and the vehicle's age and mileage can impact your financing options.

Understanding how these factors influence your monthly payment is crucial before you step onto a dealership lot. A used car loan calculator is an essential tool in this process. It allows you to experiment with different scenarios—such as increasing your down payment or securing a lower interest rate—to see exactly how they affect your bottom line. Whether you're looking at a certified pre-owned sedan or an older SUV, knowing your numbers empowers you to negotiate with confidence and avoid overextending your budget.

In this guide, we'll walk you through how to use our calculator effectively, explain the key components of a used car loan, and provide actionable tips to help you secure the best possible deal. By the end, you'll have a clear roadmap to financing your next vehicle without breaking the bank.

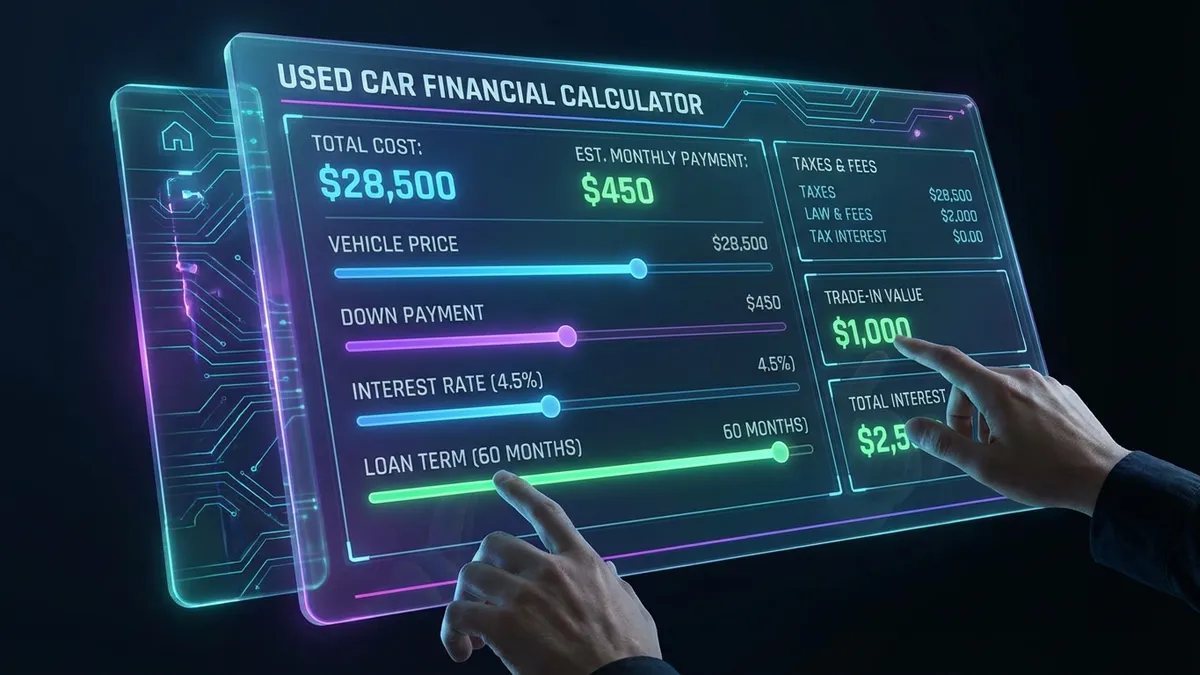

How to Use This Used Car Calculator

Our calculator is designed to be intuitive and comprehensive. Here's a step-by-step breakdown of each input field and how it impacts your results:

- Vehicle Price: Enter the sticker price of the car you're interested in. Don't forget that this is just the starting point; taxes and fees will be added later.

- Down Payment: This is the cash you pay upfront. A larger down payment reduces the amount you need to borrow, which lowers your monthly payment and total interest costs. Aim for at least 10-20% if possible.

- Trade-in Value: If you're selling your current car to the dealer, enter its estimated value here. This acts like an additional down payment, further reducing your loan principal.

- Interest Rate (APR): This is the annual percentage rate charged by the lender. Used car rates are generally higher than new car rates due to the perceived risk. Your rate will depend on your credit score and the vehicle's age.

- Loan Term: The length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72). Longer terms lower your monthly payment but increase the total interest you pay over the life of the loan.

- Sales Tax: Enter your local sales tax rate. This is often overlooked but can add thousands of dollars to the total cost of the vehicle.

As you adjust these inputs, the calculator instantly updates your estimated monthly payment, total interest paid, and the total cost of the loan. Use the donut chart to visualize how much of your total payment is going toward the principal versus interest and taxes.

Key Factors Affecting Used Car Loans

Financing a used car isn't exactly the same as financing a new one. Lenders view used cars as riskier assets because their value is harder to predict and they have a shorter remaining lifespan. Here are the main factors that will influence your loan terms:

1. Credit Score

Your credit score is the single most significant factor in determining your interest rate. Borrowers with excellent credit (720+) can qualify for rates significantly lower than those with subprime credit (below 620). Before shopping, check your credit report for errors and try to improve your score if possible. Even a 1% difference in APR can save you hundreds or thousands of dollars over the life of the loan.

2. Vehicle Age and Mileage

Lenders often have restrictions on the age and mileage of vehicles they will finance. For example, some banks won't finance cars older than 10 years or with more than 100,000 miles. Additionally, older cars typically come with higher interest rates because they depreciate faster and are more likely to break down, increasing the risk of default.

3. Loan-to-Value (LTV) Ratio

The LTV ratio compares the loan amount to the vehicle's actual value. If you're buying a car for $20,000 but it's only worth $18,000, you have a high LTV ratio (over 100%), which is risky for the lender. Making a substantial down payment helps lower the LTV ratio, making it easier to get approved and secure a better rate.

Strategies for Lowering Your Monthly Payment

If the estimated payment is higher than your budget allows, don't panic. There are several levers you can pull to bring it down to a comfortable level:

- Increase Your Down Payment: Saving up a bit longer to put more money down is the most effective way to lower your payment and save on interest.

- Shop for a Better Rate: Don't just accept the dealer's financing. Get pre-approved offers from credit unions, banks, and online lenders. Credit unions, in particular, are known for offering competitive rates on used car loans.

- Choose a Cheaper Car: It might be tough to hear, but sometimes the best financial decision is to opt for a less expensive vehicle that still meets your needs.

- Extend the Loan Term (With Caution): Stretching the loan from 48 to 60 or 72 months will lower your monthly bill, but you'll pay significantly more in interest. Only do this if absolutely necessary, and try to pay extra whenever possible to shorten the term.

Used vs. New Car Financing: What's the Difference?

It's important to understand the trade-offs between financing used versus new. New cars often come with promotional financing offers from the manufacturer, such as 0% or 1.9% APR. Used cars rarely have such incentives. As a result, the interest rate on a used car loan can be 2-4 percentage points higher than a new car loan.

However, the lower purchase price of a used car often outweighs the higher interest rate. New cars depreciate rapidly—losing up to 20% of their value in the first year. By buying used, you let the original owner take that depreciation hit. Use our Auto Loan Calculator to compare the total cost of a new car versus a used car to see which makes more financial sense for you. You can also check our Car Affordability Calculator to see what price range fits your budget. If you are buying from a distance, don't forget to factor in shipping costs.

Additional Resources

For more information on auto financing and consumer rights, check out these trusted resources:

- FTC: Financing or Leasing a Car - A comprehensive guide from the Federal Trade Commission on your rights and options when buying a car.

- CFPB: Auto Loans - Tools and advice from the Consumer Financial Protection Bureau to help you navigate the auto loan process.

Frequently Asked Questions (FAQ)

What is a good interest rate for a used car?

Interest rates vary based on the economy and your credit score. Generally, a "good" rate is anything below the national average for your credit tier. For borrowers with excellent credit, rates might be around 5-7%, while those with fair credit might see rates of 10-15% or higher.

Can I get a 72-month loan on a used car?

Yes, many lenders offer 72-month or even 84-month terms for used cars, especially if the vehicle is relatively new (less than 5 years old). However, be careful—long terms on used cars increase the risk of becoming "upside down" (owing more than the car is worth).

Does the calculator include title and registration fees?

No, this calculator focuses on the loan principal, interest, and sales tax. Title, registration, and dealer documentation fees vary widely by state and dealership. You should budget an extra $200-$500 for these costs, or ask the dealer for an estimate to add to the vehicle price.

Should I finance through a bank or the dealership?

It's best to get pre-approved by a bank or credit union before you go to the dealership. This gives you a baseline rate to compare against the dealer's offer. Dealers can sometimes beat bank rates, but having a pre-approval gives you leverage.