The Power of a Down Payment: Lower Monthly Payments & Less Interest

When buying a car, the down payment is often the single most powerful tool you have to control your financial future. Many buyers focus solely on the monthly payment, but the Car Payment Calculator With Down Payment reveals a deeper truth: putting money down upfront doesn't just lower your monthly bill—it saves you thousands of dollars in interest over the life of the loan.

In this comprehensive guide, we will explore how down payments work, why they are critical for approval and interest rates, and how to use our calculator to find the perfect balance between your upfront cash and your monthly budget.

How to Use This Calculator

Our Car Payment Calculator With Down Payment tool is designed to be simple yet powerful. Follow these steps to get an accurate estimate:

- Enter Loan Amount: Input the total amount you plan to borrow.

- Set Interest Rate: Enter the annual interest rate (APR) offered by your lender.

- Choose Loan Term: Select the duration of the loan in months (e.g., 60 months).

The Power of a Down Payment

Making a substantial down payment is one of the best ways to save money on your car loan. It reduces the principal amount you need to borrow, which in turn lowers your monthly payment and the total interest you pay over the life of the loan. It also helps you avoid being "upside-down" on your loan, where you owe more than the car is worth.

How to Use This Calculator

Our calculator is designed to show you the direct correlation between your down payment and your long-term savings. Here is how to get the most out of it:

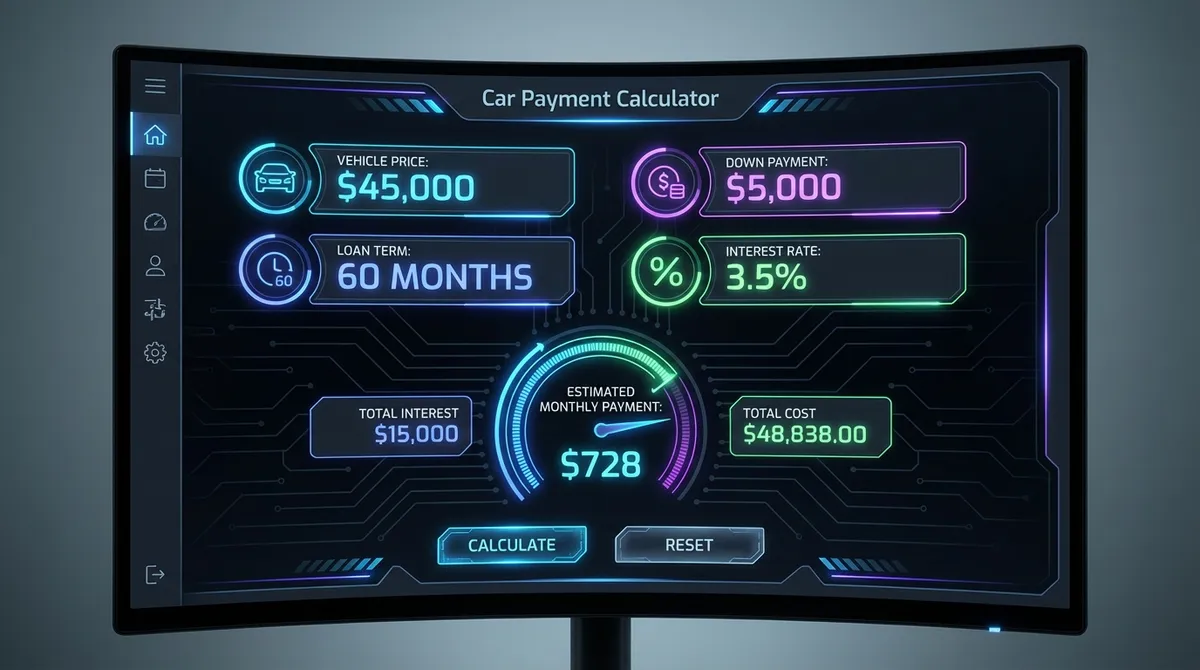

- Vehicle Price: Enter the total sticker price of the car you want to buy. Don't forget to include estimated taxes and fees if you want a true "out-the-door" calculation.

- Trade-In Value: If you are trading in an old vehicle, enter its value here. This acts exactly like a cash down payment, reducing your loan amount directly.

- Down Payment: Enter the amount of cash you plan to pay upfront. Use the slider to see how increasing this amount by just $500 or $1,000 affects your monthly payment.

- Interest Rate (APR): Enter your estimated interest rate. If you have a higher down payment, you may qualify for a lower rate—try adjusting this to see the impact.

- Loan Term: Select how many months you will be paying off the loan. Common terms are 36, 48, 60, and 72 months.

Why a Down Payment Matters: The Math Behind the Savings

A down payment is an upfront partial payment for the purchase of a vehicle. The remainder of the cost is financed through a loan. The math is simple but impactful: every dollar you put down is a dollar you don't have to borrow and, consequently, a dollar you don't pay interest on.

For example, on a $30,000 car with a 7% interest rate over 60 months:

- $0 Down: You borrow $30,000. Your monthly payment is roughly $594. Total interest paid: $5,642.

- $5,000 Down: You borrow $25,000. Your monthly payment drops to $495. Total interest paid: $4,702.

In this scenario, a $5,000 down payment saves you nearly $1,000 in interest and lowers your monthly obligation by almost $100. This "double benefit" is why financial experts always recommend putting money down.

The 20/4/10 Rule of Car Buying

If you are unsure how much to put down, consider the 20/4/10 rule. This is a classic financial guideline designed to keep you from becoming "car poor."

- 20% Down: You should aim to put down at least 20% of the car's purchase price. This protects you from depreciation (the loss of value) that happens the moment you drive off the lot.

- 4 Years (48 Months): Ideally, you should finance the car for no more than 4 years. Longer terms like 72 or 84 months might lower your payment, but they drastically increase your total interest cost.

- 10% of Income: Your total monthly car expenses (payment, insurance, gas, maintenance) should not exceed 10% of your gross monthly income.

While 20% is the gold standard, it isn't always possible for everyone. Even a 10% down payment is significantly better than zero. Use our calculator to test different scenarios and see what fits your budget.

Avoiding "Gap Insurance" with a Down Payment

One hidden benefit of a substantial down payment is avoiding the need for Gap Insurance. Gap insurance covers the difference between what your car is worth and what you owe on the loan if your car is totaled.

If you put $0 down, you are almost immediately "underwater" or having "negative equity"—meaning you owe more than the car is worth—because new cars depreciate by about 10-20% in the first year. If you total the car, your standard insurance will only pay the market value, leaving you to pay the rest of the loan out of pocket unless you have Gap Insurance.

By putting 20% down, you ensure that your loan balance is always lower than the car's value, effectively self-insuring against this risk and saving you the cost of a Gap policy.

Common Down Payment Myths

There are several misconceptions about down payments that can cost buyers money. Let's debunk a few:

Myth 1: "I should keep my cash and invest it instead."

Reality: Unless your investment returns are guaranteed to be higher than your auto loan interest rate (after taxes), this is risky. With auto loan rates often hovering around 6-9% for new cars and higher for used, paying down the loan is a guaranteed "return" of that percentage.

Myth 2: "I can just refinance later."

Reality: Refinancing is never guaranteed. If your credit score drops or your car's value plummets (negative equity), you may not be able to refinance at all. It is safer to structure the loan correctly from the start.

Myth 3: "Zero down deals are always better."

Reality: "Zero Down" deals are marketing tactics to get you into a car. They often come with higher interest rates or are restricted to specific, less popular models. Always read the fine print and calculate the Total Cost of Loan before signing.

Frequently Asked Questions

External Resources

For more information on auto financing and down payments, check out these trusted resources:

- CFPB: Auto Loans Guide - Official government guide to understanding auto loans.

- Investopedia: Down Payment Definition - A financial breakdown of how down payments work.