Mastering Your Car Calculator Payment: A Complete Guide

Navigating the world of auto financing can be daunting, but understanding your car calculator payment is the first step toward making a financially sound decision. Whether you are eyeing a brand-new sports car or a reliable used sedan, knowing exactly how much you will pay each month—and over the life of the loan—is crucial. This comprehensive guide will walk you through everything you need to know about calculating car payments, understanding the factors that influence them, and strategies to keep your costs low.

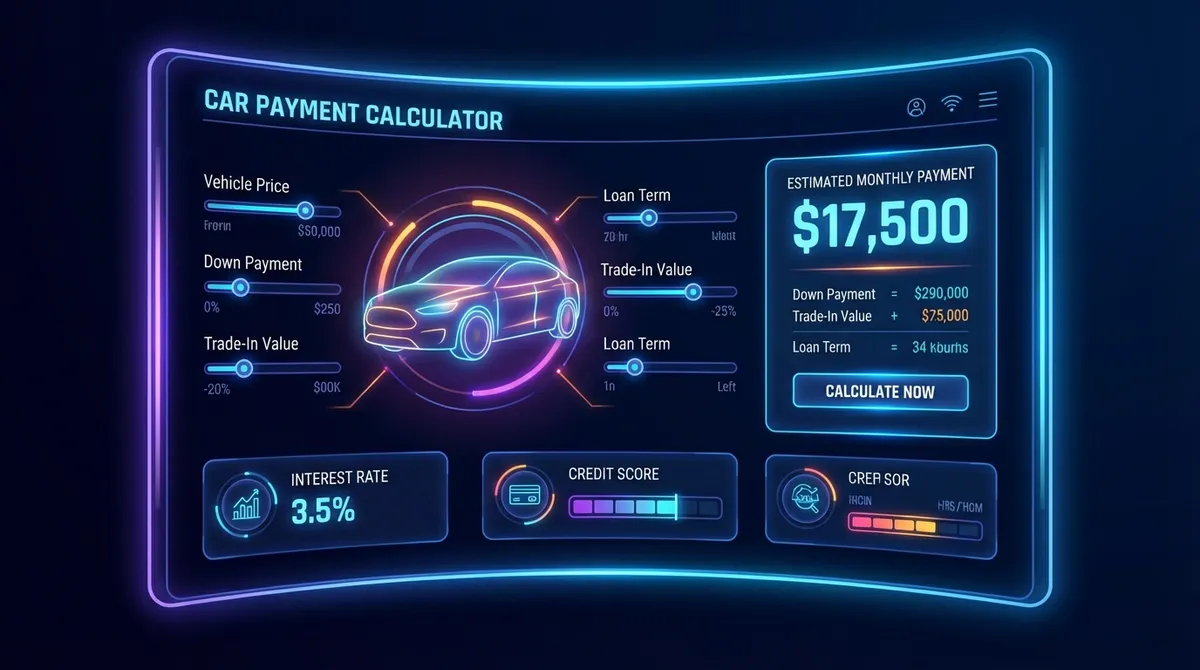

Our advanced Car Calculator Payment tool is designed to give you a clear, detailed picture of your potential auto loan. By inputting key variables like vehicle price, down payment, trade-in value, and interest rate, you can instantly see your estimated monthly payment, total interest paid, and the total cost of the vehicle. This empowers you to negotiate better terms and choose a car that fits comfortably within your budget.

How to Use This Car Calculator Payment Tool

Getting the most accurate results from our calculator is simple. Here is a step-by-step breakdown of each input field and why it matters:

- Vehicle Price: Enter the total purchase price of the car. This should include the sticker price plus any dealer add-ons or options you plan to include. Do not include sales tax or fees here; there are separate fields for those.

- Down Payment: This is the amount of cash you are paying upfront. A larger down payment reduces the loan amount, which in turn lowers your monthly payment and the total interest you will pay over the life of the loan.

- Trade-in Value: If you are trading in an old vehicle, enter its estimated value here. This amount is deducted from the vehicle price, further reducing the amount you need to finance.

- Interest Rate (APR): Enter the annual percentage rate (APR) you expect to receive from a lender. This rate is determined by your credit score, the loan term, and current market conditions.

- Loan Term: Select the number of months you will be paying off the loan. Common terms are 36, 48, 60, 72, and 84 months. Longer terms lower your monthly payment but increase the total interest paid.

- Sales Tax: Enter your state or local sales tax rate. This is a significant cost that is often overlooked but must be financed if not paid upfront.

- Fees: Include any dealer documentation fees, registration costs, or other administrative charges. These can add up to hundreds of dollars.

Understanding the Components of Your Monthly Payment

Your monthly car payment is not just a random number; it is composed of three primary elements: principal, interest, and sometimes taxes and fees. Understanding how these work together is key to mastering your car calculator payment.

1. Principal

The principal is the actual amount of money you borrowed to buy the car. Each month, a portion of your payment goes toward reducing this balance. In the early stages of your loan, a smaller percentage of your payment goes to principal compared to the end of the loan term.

2. Interest

Interest is the cost of borrowing money. It is calculated based on your remaining principal balance and your APR. In the beginning, your interest payments are higher because your principal balance is highest. As you pay down the loan, the interest portion of your monthly payment decreases.

3. Taxes and Fees

While often paid upfront, many buyers choose to roll sales tax and dealer fees into their loan. If you do this, you are paying interest on these costs as well, which increases your monthly payment and total loan cost.

Factors That Influence Your Car Payment

Several variables can drastically change your monthly payment. Being aware of these can help you strategize for a better deal.

- Credit Score: Your credit score is the single most significant factor affecting your interest rate. A higher score qualifies you for lower rates, which can save you thousands of dollars over the life of the loan.

- Loan Term Length: extending your loan term from 60 to 84 months will lower your monthly payment, but it will significantly increase the total interest you pay. It also puts you at higher risk of becoming "upside-down" on your loan (owing more than the car is worth).

- Down Payment Size: The more you put down, the less you borrow. A substantial down payment (aim for at least 20%) provides a buffer against depreciation and lowers your monthly obligation.

- Vehicle Choice: New cars often come with lower interest rates (sometimes even 0% APR promotions) compared to used cars, but they also have higher price tags and faster depreciation.

Pro Tips to Lower Your Monthly Payment

If the estimated payment from our car calculator payment tool is higher than you would like, consider these strategies to bring it down:

- Improve Your Credit Score: Before applying for a loan, check your credit report for errors and pay down existing debt. Even a small increase in your score can drop your rate by a percentage point or more.

- Shop Around for Financing: Don't just accept the dealer's offer. Get pre-approved by a bank, credit union, or online lender. Having a pre-approval in hand gives you leverage at the dealership.

- Increase Your Down Payment: Save up a bit longer if possible. Every extra dollar you put down is a dollar you don't have to pay interest on.

- Consider a Cheaper Car: It might be tough to hear, but sometimes the best way to lower your payment is to choose a less expensive vehicle or a reliable used model.

- Refinance Later: If you are stuck with a high rate now, make on-time payments for 6-12 months to improve your credit, then look into refinancing for a lower rate.

Common Mistakes to Avoid

When using a car calculator payment tool and shopping for a loan, avoid these common pitfalls:

- Focusing Only on Monthly Payment: Dealers often ask, "What monthly payment do you want?" They can manipulate the loan term to hit that number while charging you a higher price or interest rate. Always negotiate the total "out-the-door" price of the car first.

- Ignoring Total Cost: A long-term loan might look affordable monthly, but calculate the total cost (Principal + Interest). You might end up paying double the car's value.

- Forgetting Insurance and Maintenance: Your car payment is only part of the cost of ownership. Make sure you budget for insurance premiums, fuel, and regular maintenance.

- Rolling in Negative Equity: If you owe more on your trade-in than it's worth, rolling that balance into your new loan is a recipe for financial disaster. It creates a cycle of debt that is hard to escape.

External Resources

For more information on auto loans and managing your finances, check out these helpful resources:

- Consumer Financial Protection Bureau: Auto Loans - A government guide to understanding auto loans.

- Investopedia: Amortization Explained - Learn how loan amortization works.